A salvage title is a permanent legal designation showing that a classic car was declared a total loss by an insurance company. Understanding what is a salvage title classic car is the first step every collector must take before signing any purchase agreement. The designation affects resale value, insurance options, financing access, and long-term collector appeal. This guide breaks down exactly how salvage titles work, how they differ from rebuilt and clean titles, and what you need to check before buying a classic car with one.

What is a salvage title classic car?

A salvage title is issued when an insurance company declares a vehicle a total loss because repair costs exceed a set threshold of the car's pre-damage market value. That threshold typically falls between 60% and 90%, depending on the state. Once issued, the salvage brand is permanent. It stays on the vehicle's record forever, even if the car is fully restored.

For classic cars, this designation carries extra weight. A 1969 Chevrolet Camaro or a 1965 Ford Mustang with a salvage title is not just a damaged car. It is a vehicle whose collector status, insurance eligibility, and resale potential are all permanently altered. The title brand follows the car through every future sale, showing up in databases like Carfax and NMVTIS.

A salvage title also means the car is not legal to drive on public roads in its current state. You cannot register it, insure it for road use, or drive it to a show until it clears a state inspection and receives a rebuilt title.

How are salvage titles assigned?

State rules vary widely on what triggers a salvage title. There is no single national standard. Each state sets its own total loss threshold, and insurers apply their own formulas within those rules.

Common damage types that trigger a salvage title include:

- Collision damage where frame or structural repair costs exceed the threshold

- Flood damage, which is especially destructive to electrical systems and floor pans

- Fire damage, which can compromise wiring, fuel systems, and body panels

- Theft recovery, where the vehicle was written off before being found

- Hail damage severe enough to total the vehicle on paper, even if it still runs

The insurance company, not the state DMV, makes the initial total loss call. The DMV then issues the salvage brand on the title based on that declaration. This means two identical 1970 Dodge Chargers with the same damage could receive different outcomes depending on which state they are registered in.

Pro Tip: Always ask which state issued the salvage title. A state with a low total loss threshold, like Texas at 100% of market value, may brand a car salvage for damage that another state would not.

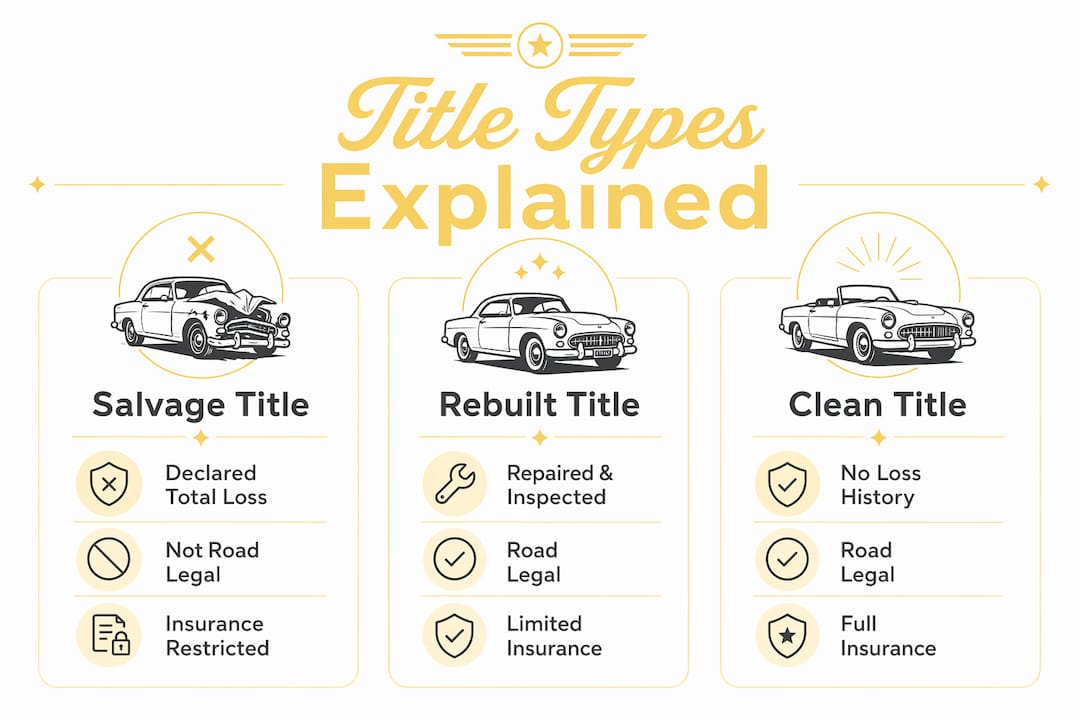

Salvage title vs. rebuilt title vs. clean title

These three designations mean very different things. Confusing them is one of the most common and costly mistakes classic car buyers make.

| Title Type | Meaning | Road Legal? | Insurance Impact |

|---|---|---|---|

| Salvage | Declared total loss; not roadworthy | No | Not insurable for road use |

| Rebuilt | Repaired and passed state inspection | Yes | Limited coverage available |

| Clean | No total loss event on record | Yes | Full coverage available |

A salvage title means the car has been declared a total loss and cannot legally be driven. A rebuilt title is issued after the owner completes documented repairs and passes a state-mandated inspection. That inspection confirms the car is minimally roadworthy. It does not confirm the car meets factory safety standards or original quality.

A clean title means no total loss event has ever been recorded on that vehicle. For collector cars, a clean title is the gold standard. It directly supports higher resale prices and full insurance coverage.

Pro Tip: A rebuilt title is not a clean title. The salvage history remains visible in every vehicle history report, permanently affecting collector value even after a flawless restoration.

What are the real implications of buying a salvage title classic car?

Buying a classic car with a salvage title carries financial, legal, and practical consequences that go well beyond the purchase price.

-

Value drop. Vehicles with salvage history sell for 20% to 40% less than comparable clean-title cars. For a collector-grade vehicle worth $80,000 with a clean title, that gap could mean $16,000 to $32,000 in lost value at resale.

-

Insurance restrictions. Many major insurers limit coverage on salvage-branded vehicles to liability only. That means no comprehensive coverage for fire, theft, or weather damage. For a classic car stored in a garage or shown at events, that gap in protection is serious.

-

Financing challenges. Lenders often refuse to finance salvage or rebuilt vehicles outright. When they do approve a loan, buyers face larger down payments and higher interest rates. This limits your buyer pool at resale too, since future buyers face the same lending walls.

-

Hidden damage risk. The full extent of original damage may never be fully known. Structural damage, flood corrosion, or fire-related wiring issues can hide behind fresh paint and new upholstery. You carry the full financial risk if problems surface after purchase.

-

Registration and inspection hurdles. A salvage title car must be repaired and pass inspection to receive a rebuilt title before it can be registered. Some states require inspections by certified agencies, not just a general mechanic.

"Buying salvage title vehicles is considered risky due to unknown original damage and repair quality. Buyers carry the full financial risk if problems are hidden." — NerdWallet

Understanding classic car insurance value is especially critical here. Standard auto policies and specialty classic car policies treat salvage history very differently.

How do you evaluate a salvage title classic car before buying?

Smart buyers treat a salvage title classic car like a puzzle. Your job is to find every missing piece before you commit.

- Request the original insurance adjuster's damage report. This document describes the damage that triggered the total loss declaration. It tells you what the insurer saw, not what the seller is telling you.

- Get full repair documentation. Ask for receipts, parts invoices, and before-and-after photos. A legitimate restoration will have a paper trail. No documentation is a red flag.

- Run a vehicle history report. Services like Carfax and NMVTIS confirm the salvage branding and show any additional title events, ownership changes, or odometer discrepancies.

- Hire a specialist inspector. A general mechanic is not enough. You need someone who knows classic car construction and can assess structural integrity, frame alignment, and period-correct electrical systems.

- Check your state's rules. Review state-specific salvage regulations before buying. What is legal to register in one state may require additional inspections in another.

Pro Tip: Use the Butterclassics dealer inspection checklist as a starting framework when evaluating any classic car with a complex title history.

Reviewing title work in classic car sales before you buy is one of the most practical steps you can take. Title issues discovered after purchase are far more expensive to resolve.

Key Takeaways

A salvage title is a permanent brand that reduces a classic car's value, limits insurance options, and complicates financing regardless of how well the vehicle has been restored.

| Point | Details |

|---|---|

| Salvage title is permanent | The brand stays on vehicle history reports forever, even after a rebuilt title is issued. |

| Value drops significantly | Salvage-history classics sell for 20% to 40% less than clean-title equivalents. |

| Insurance is restricted | Most insurers limit salvage-title cars to liability coverage only, excluding theft and collision. |

| Financing is harder | Lenders often refuse loans on salvage vehicles or require larger down payments. |

| Inspection is non-negotiable | Always get a specialist inspection and full repair documentation before purchasing. |

My honest take on salvage title classics

I have seen collectors fall hard for a beautiful restoration, only to discover the salvage title made the car nearly impossible to insure properly or sell at a fair price years later. The car looked perfect. The paperwork told a different story.

Here is what experience teaches you: a salvage title is not just a discount. It is a permanent condition that follows the car into every future transaction. Even a frame-off restoration by a top shop cannot erase the salvage brand from Carfax or NMVTIS. Buyers at resale will see it. Insurers will see it. Lenders will see it.

That said, salvage title classics are not always a bad deal. For an experienced restorer who wants a project car and has no plans to resell, the 20% to 40% price discount can make a rare model accessible. A 1967 Shelby GT500 with flood damage might be the only way some collectors ever get near one. The math can work if you go in with clear eyes.

The buyers who get hurt are the ones who treat a salvage title as a minor footnote. They focus on the chrome and the paint and skip the structural inspection. They assume a rebuilt title means the car is "as good as new." It is not. A rebuilt title only confirms minimal roadworthiness, not factory-original quality.

My advice: if you are newer to collecting, stick with clean-title cars. If you are experienced and know how to evaluate damage, a salvage title classic can be a calculated opportunity. Just never skip the specialist inspection, and always read the adjuster's report before you fall in love with the car.

— Tony

Classic cars worth collecting, with no guesswork

Butterclassics carries a hand-picked inventory of classic and vintage vehicles, from muscle cars and Corvettes to Broncos and vintage trucks. If you want the confidence of a verified vehicle, the Butter Certified program gives you documented quality assurance before you buy.

For buyers open to restoration projects, Butterclassics also lists salvage title classics where the history is fully disclosed. You get the details upfront, not after the fact. Browse the full classic car inventory and connect with the Butterclassics team for personalized guidance on any vehicle, certified or project-grade.

FAQ

What does a salvage title mean on a classic car?

A salvage title means the vehicle was declared a total loss by an insurance company because repair costs exceeded a state-set threshold, typically 60% to 90% of its pre-damage value. The brand is permanent and appears on all future vehicle history reports.

Can you insure a classic car with a salvage title?

Most major insurers restrict coverage on salvage-title vehicles to liability only, excluding comprehensive and collision coverage. Full classic car insurance is generally only available on clean or rebuilt-title vehicles.

Is a rebuilt title the same as a clean title?

No. A rebuilt title means the car passed a state inspection after repairs, confirming it is roadworthy. A clean title means no total loss event was ever recorded. The salvage history remains visible in databases even after a rebuilt title is issued.

How much less is a salvage title classic car worth?

Vehicles with salvage history typically sell for 20% to 40% less than comparable clean-title cars. For high-value collector cars, that gap can represent tens of thousands of dollars at resale.

Can you get financing for a salvage title classic car?

Financing is difficult. Many lenders refuse loans on salvage or rebuilt vehicles entirely. When financing is available, buyers typically face larger down payments and higher interest rates than they would on a clean-title vehicle.