If you own a classic car, standard auto insurance is probably working against you. Classic car insurance value explained simply means this: your vintage vehicle deserves a policy that reflects what it's actually worth, not what it has depreciated to. Most collectors don't realize that a standard policy pays out based on depreciated market value, which can leave you thousands of dollars short after a total loss. Getting this right protects your investment, your passion, and your peace of mind.

Table of Contents

- Key takeaways

- Classic car insurance value explained: agreed value vs. ACV

- What affects your classic car insurance rates

- How to value your classic car for insurance

- What to expect when you file a claim

- My honest take on classic car insurance

- Find your next classic at Butterclassics

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Agreed value beats ACV | Agreed value policies guarantee a pre-set payout with no depreciation deducted at claim time. |

| Classic insurance costs less | Classic car policies typically run $200 to $600 per year, far below standard auto insurance rates. |

| Appraisals set your coverage | A professional appraisal using USPAP standards gives you a defensible, accurate agreed value. |

| Accurate reporting matters | Misreporting mileage or storage conditions is one of the most common reasons claims get denied. |

| Update your value regularly | Classic car markets shift fast, so revisit your agreed value every one to two years. |

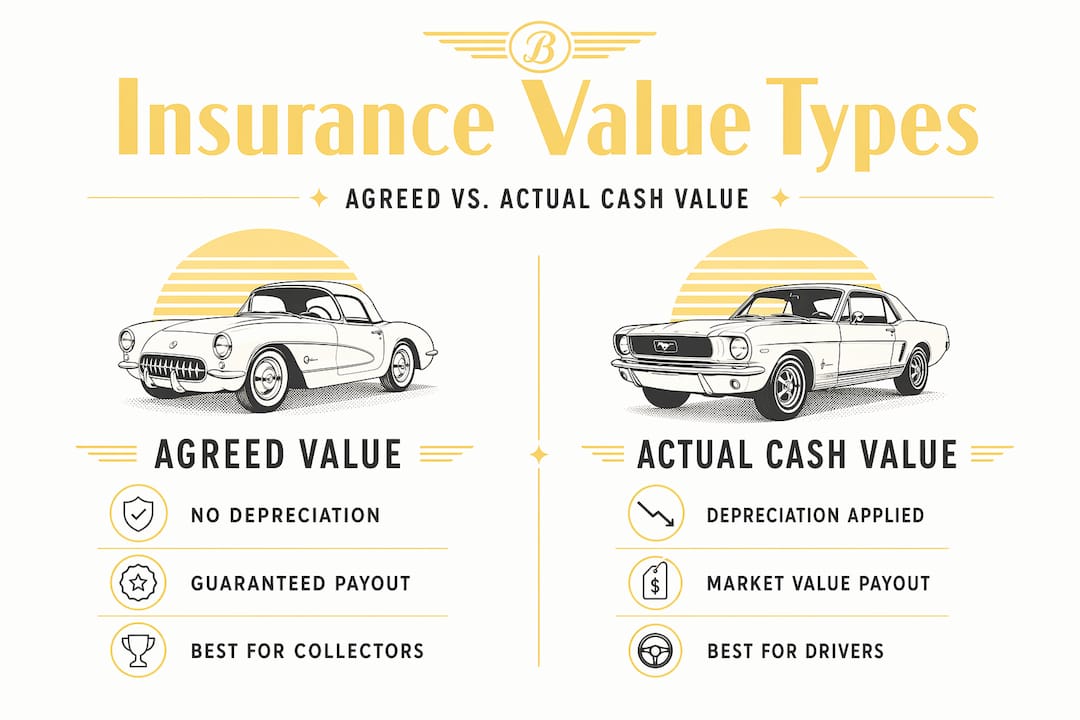

Classic car insurance value explained: agreed value vs. ACV

Not all insurance policies treat your car the same way. Standard auto insurance typically pays out based on actual cash value (ACV), which factors in depreciation. For a 1969 Camaro that has appreciated in value over decades, ACV is a disaster waiting to happen.

Classic car insurance works differently. There are three valuation methods you need to know:

- Actual Cash Value (ACV): The insurer pays what your car was worth on the open market right before the loss, minus depreciation. This is standard auto insurance territory, and it almost always shortchanges collectors.

- Stated Value: You declare a value, and the policy sets that as a ceiling. The catch? The insurer can still apply depreciation and pay less than your stated amount. Stated value policies create a false sense of security because the insurer may pay below the stated ceiling based on ACV calculations.

- Agreed Value: You and the insurer agree upfront on a specific dollar amount, backed by documentation and a professional appraisal. If the car is a total loss, agreed value guarantees that exact payout. No depreciation. No negotiation. No surprises.

For collectors, agreed value is the only method that makes real sense. It removes ambiguity from the claims process entirely.

Pro Tip: Ask your insurer directly whether your policy is "agreed value" or "stated value." Those two terms sound similar but function very differently when it comes to a claim payout.

Here is a quick side-by-side comparison to make it crystal clear:

| Policy Type | Depreciation Applied? | Payout Guarantee? | Best For |

|---|---|---|---|

| Actual Cash Value | Yes | No | Standard daily drivers |

| Stated Value | Possibly | No | Some collector vehicles |

| Agreed Value | No | Yes | Classic and collector cars |

The classic car insurance appraisal process involves submitting documentation, photos, and a professional appraisal to establish that agreed figure. Once both parties sign off, that number is locked in.

What affects your classic car insurance rates

Here is something that surprises most people: classic car insurance is often much cheaper than standard coverage. Classic policies typically cost $200 to $600 annually, compared to the average standard auto insurance cost of $2,329 to $2,697 per year in 2026. That is a significant difference.

Why the lower cost? Classic car owners tend to drive their vehicles far less, store them carefully, and treat them with more care than a daily commuter car. Insurers recognize that lower risk and price accordingly.

That said, several factors still influence what you pay:

- Vehicle value: A $150,000 restored Shelby Cobra costs more to insure than a $25,000 project car. The agreed value you set directly affects your premium.

- Annual mileage: Most classic car policies include mileage caps, often 2,500 to 7,500 miles per year. Staying within those limits keeps your rate low.

- Storage conditions: A climate-controlled garage is a very different risk than a gravel lot. Insurers reward secure, enclosed storage with better rates.

- Driving record: Your personal history still matters. A clean record keeps premiums in check.

- Location: Urban areas with higher theft rates or weather risks push premiums up.

- Number of vehicles: Multi-vehicle discounts are common, especially if you insure a collection.

Premium factors including mileage, storage, and vehicle value all work together to determine your final rate. The good news is that most of these factors are within your control.

Pro Tip: If you store your classic in a locked, climate-controlled garage and drive it fewer than 3,000 miles per year, mention both details explicitly when getting quotes. Those two factors alone can meaningfully reduce your premium.

How to value your classic car for insurance

Getting the right agreed value starts with an honest, professional assessment of your vehicle. This is where a lot of collectors make costly mistakes. Some set values too low to save on premiums. Others rely on emotional attachment rather than market data. Both approaches can hurt you badly when a claim comes in.

Here is a practical process for valuing your classic car correctly:

-

Hire a certified appraiser. Look for appraisers who follow USPAP appraisal standards, which are the recognized professional benchmarks for defensible, documented valuations. A USPAP-compliant appraisal gives your insurer confidence and protects you in a dispute.

-

Document everything. Photographs, receipts, restoration records, and service history all support your agreed value. If you spent $30,000 restoring an engine, that needs to be reflected in your coverage.

-

Include modifications and custom work. A stock 1967 Mustang and a fully restored, custom-painted show car with upgraded suspension are not worth the same amount. Make sure your policy covers what the car actually is today, not what it was from the factory.

-

Avoid setting value too low. Undervaluing your car to reduce premiums is a false economy. If your agreed value is $40,000 but replacement cost is $65,000, you are absorbing a $25,000 loss out of pocket after a total loss claim.

-

Revisit your appraisal every one to two years. Classic car markets move. A car that was worth $50,000 in 2023 may be worth $70,000 today. Stale valuations leave real money on the table.

One more thing worth knowing: you can browse certified classic vehicles to get a realistic sense of current market values for specific makes and models. Real transaction data beats guesswork every time.

Pro Tip: When getting a new appraisal, bring your previous one along. A side-by-side comparison helps the appraiser identify exactly what has changed in value and why, making the new document more thorough.

What to expect when you file a claim

One of the biggest advantages of agreed value coverage is how much smoother the claims process becomes. With a standard ACV policy, you are often negotiating with an adjuster who has every incentive to minimize the payout. With agreed value, that argument does not exist.

Here is what the claims experience looks like with proper classic car coverage:

- Guaranteed payout amount. Agreed value claims pay the full pre-set amount with no depreciation deducted. If your agreed value is $60,000, that is what you receive on a total loss.

- Faster settlements. Because the value is already established and documented, there is far less back-and-forth. Settlements tend to move quicker and with less friction.

- Choice of repair shop. Many classic car policies let you select a specialist restoration shop rather than sending your vehicle to a generic body shop. That matters enormously for rare or custom vehicles.

- Coverage for spare parts and restorations. Quality classic car policies often extend coverage to spare parts, tools, and ongoing restoration work. Check your policy details carefully.

- Organized documentation speeds everything up. Keep your appraisal, photos, receipts, and policy documents in one place. When you need them, you will want them immediately.

Accurate mileage and usage declarations are also critical here. Misreporting how you use the car or where it is stored is one of the most common reasons claims get denied. Be honest upfront. It protects you later.

My honest take on classic car insurance

I have seen collectors pour years of work and serious money into a vehicle, then insure it for whatever number seemed reasonable at the time. That approach almost always ends badly.

In my experience, the biggest mistake is treating insurance as an afterthought. You spend months sourcing the right parts, finding the right restoration shop, tracking down matching-numbers components. Then you grab a quick policy without a proper appraisal and call it done. That gap between what you paid and what your policy covers is where collectors get hurt the most.

What I have learned is that working with a specialty insurer and a certified appraiser is not optional if you are serious about protecting your investment. AI-driven valuation tools are starting to change how insurers manage asset values in real time, which is genuinely exciting. But technology does not replace the need for accurate, honest documentation on your end.

The collectors who come out ahead are the ones who treat insurance as part of the ownership experience, not a checkbox. Get the appraisal. Set a realistic agreed value. Update it regularly. And never underreport your mileage or storage conditions to shave a few dollars off your premium. The short-term savings are not worth the long-term risk.

— Tony

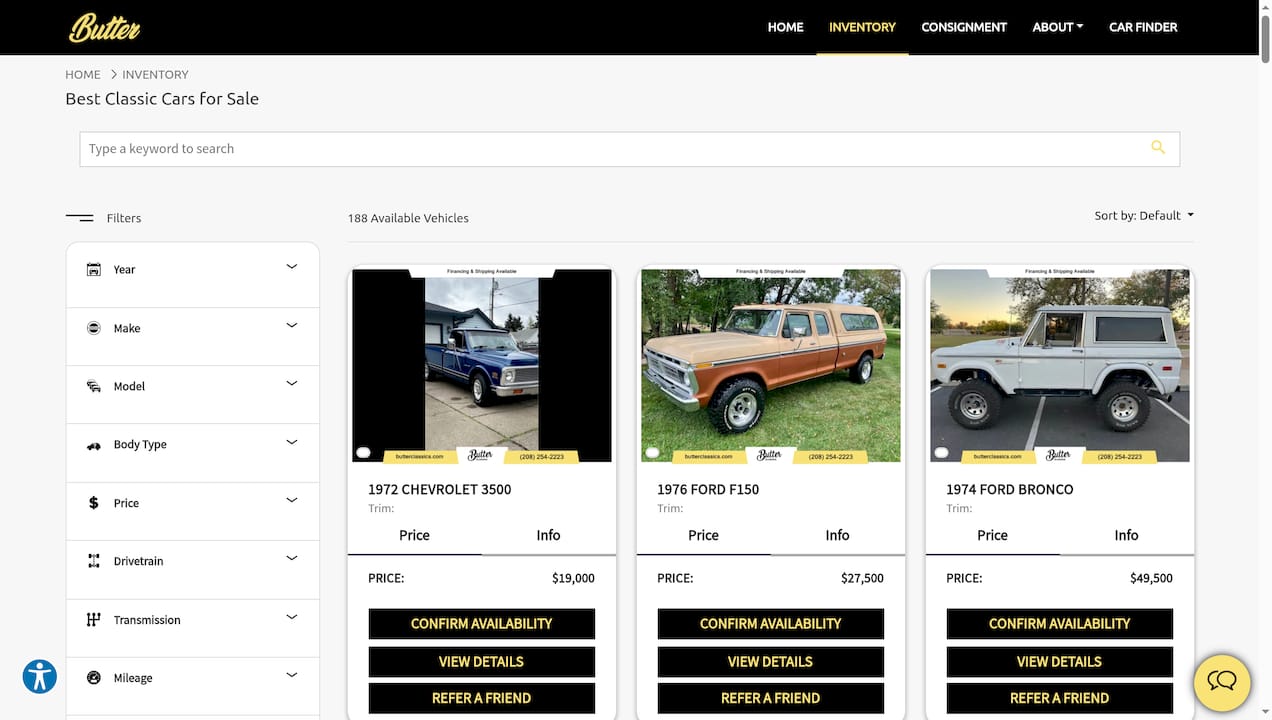

Find your next classic at Butterclassics

At Butterclassics, we know that protecting a classic car starts with knowing exactly what you have. Our inventory features a hand-picked selection of collector-grade vehicles, from muscle cars and Corvettes to vintage Broncos and trucks, each with the kind of detail and transparency that makes insurance conversations much easier.

Whether you are buying your first classic or adding to a growing collection, explore our full inventory to find vehicles with clear documentation and verified histories. Buyers who start with a well-documented car have a much smoother path to getting the right agreed value coverage from day one. Check out our Butter Certified vehicles for options that come with added confidence baked right in.

FAQ

What is classic car insurance?

Classic car insurance is a specialty policy designed for vintage and collector vehicles. Unlike standard auto insurance, it typically uses agreed value coverage, which guarantees a pre-set payout with no depreciation applied at claim time.

How does agreed value differ from stated value?

Agreed value locks in a specific payout amount that both you and the insurer confirm upfront. Stated value sets a ceiling but still allows the insurer to pay less based on actual cash value, which can leave you undercompensated.

How much does classic car insurance cost?

Classic car insurance typically costs $200 to $600 per year, which is significantly less than the $2,329 to $2,697 average for standard auto insurance in 2026. Lower mileage and careful storage are the main reasons for the lower cost.

How do I get an accurate value for my classic car?

Hire a certified appraiser who follows USPAP standards, document all restoration work and modifications, and revisit the appraisal every one to two years to keep pace with market changes.

Can I lose my claim if I misreport mileage or storage?

Yes. Misreporting mileage or storage conditions is one of the most common reasons insurers deny claims or void policies entirely. Always report accurate usage information when setting up your policy.