Classic car investment is defined as the purchase of collectible vehicles as appreciating assets, and the data shows it consistently trails the S&P 500 in raw annualized returns. That gap matters for any investor weighing classic car versus stock market returns as part of a broader portfolio strategy. Classic cars averaged roughly 4.6% annualized between 2018 and 2023, while the S&P 500 delivered approximately 10% over the same period. The real story, though, is not just the return gap. It is the tax treatment, carrying costs, liquidity constraints, and diversification benefits that determine whether a classic car belongs in your portfolio at all.

How do classic car returns compare to stock market returns?

The numbers tell a clear story. Classic cars returned ~4.6% annually between 2018 and 2023, compared to roughly 10% for the S&P 500 over the same window. That is a meaningful gap for any investor running a stock market performance comparison.

The HAGI Top Index, which tracks blue-chip collector vehicles, returned approximately 8% nominal per year since 2007. That figure looks more competitive, but it covers only the most desirable, investment-grade models. Most collectors do not own a 1962 Ferrari 250 GTO or a Gulf-liveried Ford GT40. They own vehicles that track closer to the 4.6% average.

The 2022–2024 down-cycle hit the market hard, with many models dropping 20–30% in value. Short-term holders who bought at 2021 peak prices absorbed real losses. As of april 2026, only 27% of tracked vehicles had regained positive year-over-year momentum.

| Metric | Classic Cars | S&P 500 |

|---|---|---|

| Annualized return (2018–2023) | ~4.6% | ~10% |

| HAGI Top Index (since 2007) | ~8% nominal p.a. | N/A |

| Liquidity | 4–12 weeks to sell | Instant |

| Correlation to equities | Low | N/A |

| Capital gains tax rate | Up to 28% | 15–20% |

Classic cars have low correlation with stocks and bonds, which is the real diversification argument. During equity downturns, collector car values do not necessarily move in lockstep with your brokerage account. That characteristic is worth something, even if the headline return looks modest.

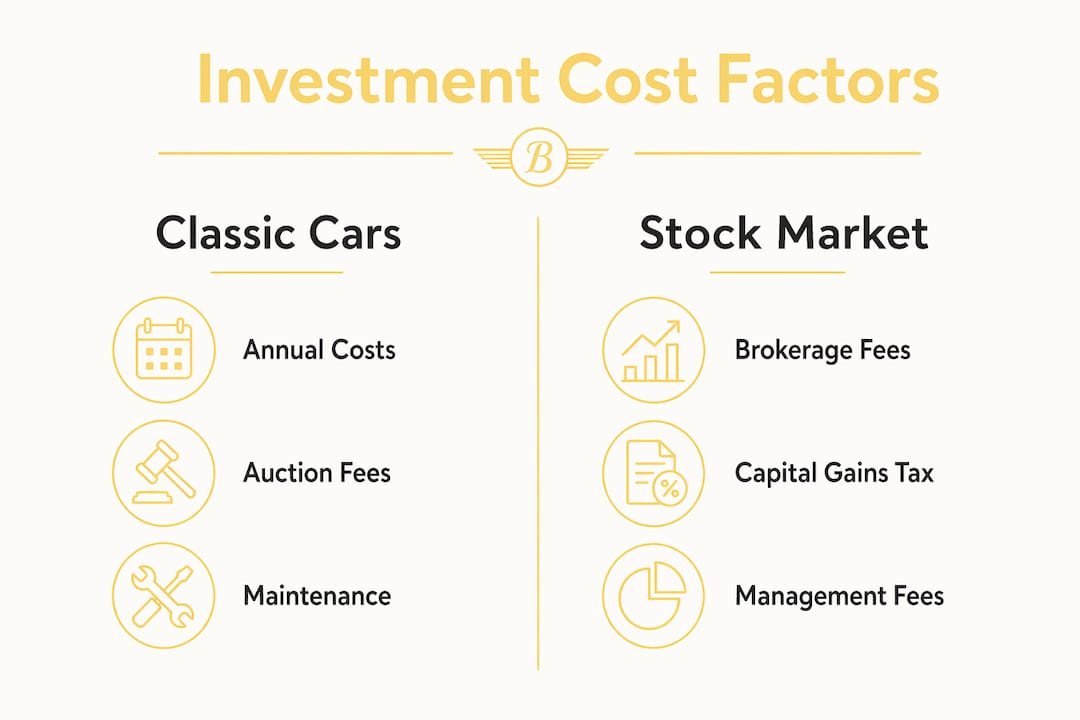

What hidden costs eat into classic car investment returns?

The biggest trap in classic car investment is underestimating total ownership costs. Annual carrying costs run 2–4% of vehicle value when you add up storage, insurance, and maintenance. On a $200,000 car, that is $4,000–$8,000 per year before you sell a single bolt.

Auction fees compound the problem. Selling through Barrett-Jackson, Mecum, or RM Sotheby's typically costs 10–15% in combined buyer and seller premiums. That fee comes straight off your net return. A car that appreciated 20% over five years can net you far less than you expect once fees are factored in.

Restoration risk is the most underappreciated danger. A poor or over-restoration can destroy 30–50% of an investment-grade car's value compared to original condition. Collectors and appraisers prize matching numbers and factory originality. A respray in the wrong color or a non-original engine swap can permanently impair value.

Common ownership costs and risks to budget for:

- Storage: Climate-controlled facilities run $200–$600 per month depending on location

- Insurance: Agreed-value policies through Hagerty or Grundy typically cost 1–2% of insured value annually

- Maintenance: Mechanical upkeep, fluid changes, and tire replacement add up fast on vehicles with aging rubber and seals

- Auction fees: 10–15% combined at major houses

- Restoration risk: Poor work destroys 30–50% of value; always use marque-specific specialists

- Liquidity delay: Standard vehicles take 4–8 weeks to sell; top models can take 6–12 months

Pro Tip: Before buying any classic car as an investment, calculate your total cost of ownership over a five-year hold. Add carrying costs, projected auction fees, and a restoration reserve. Then compare that net figure to what a simple S&P 500 index fund would return over the same period. The math often surprises people.

How does taxation differ for classic cars vs. stocks?

Tax treatment is where classic cars as assets take a significant hit relative to equities. The IRS classifies classic cars as collectibles, which means long-term capital gains are taxed at up to 28%. Stocks held longer than one year qualify for the preferential 15–20% long-term capital gains rate. That 8–13 percentage point difference directly reduces your net return.

The 2017 Tax Cuts and Jobs Act eliminated 1031 like-kind exchanges for personal property, including vehicles. Before 2018, investors could defer capital gains by rolling proceeds from one classic car sale into another. That option no longer exists. Every sale is now a taxable event with no deferral mechanism available.

Key tax differences at a glance:

- Classic cars: Up to 28% capital gains tax as collectibles under IRS rules

- Stocks: 15–20% long-term capital gains rate for most investors

- 1031 exchanges: No longer available for vehicles after the 2017 Tax Cuts and Jobs Act

- State taxes: Several states add their own capital gains layer on top of federal rates, which varies significantly

Pro Tip: Factor in your marginal tax rate before you sell. If you are in a high federal bracket, the 28% collectibles rate on a classic car sale can eliminate a large portion of your nominal gain. Talk to a CPA who understands collectible asset taxation before you list any vehicle.

What portfolio strategies work best for classic car investors?

Smart allocation is the foundation of returns on classic car investments. Prudent diversification across classic cars requires roughly $500,000 spread across 3–5 vehicles. That threshold gives you enough exposure to benefit from price variation across models and eras without concentrating risk in a single car. For investors below that threshold, professional classic car investment funds require a minimum of $125,000 and offer broader portfolio exposure with active management.

Holding period matters enormously. The recommended hold is 5–7 years to overcome carrying costs and give the market time to recognize value appreciation. Investors who bought in 2019 and sold in 2022 at peak prices did well. Those who bought at the 2021 peak and tried to exit in 2023 absorbed the brunt of the down-cycle.

JP Morgan's private banking team notes that blue-chip collector vehicles now have sophisticated pricing benchmarks and market infrastructure. That institutional recognition means classic cars can be evaluated as a niche asset class rather than purely a passion purchase. It also means price discovery is improving, which benefits serious investors.

| Ownership Type | Entry Cost | Liquidity | Management Burden | Return Potential |

|---|---|---|---|---|

| Direct ownership | $50,000+ per vehicle | Low (weeks to months) | High | 4–8% nominal |

| Classic car fund | $125,000 minimum | Medium | Low | Varies by fund |

| S&P 500 index fund | Any amount | Instant | None | ~10% historical |

The diversification benefit is real and measurable. Classic cars have low correlation with equities and bonds, which means they can reduce overall portfolio volatility during equity market downturns. For high-net-worth investors, that stability has genuine value beyond the headline return number. You can also check the 2026 market trends checklist to understand which segments are recovering fastest after the recent down-cycle.

Pro Tip: Treat classic cars as the 5–10% alternative asset slice of a diversified portfolio, not as a replacement for equities. The goal is non-correlated stability, not outperforming the S&P 500. That framing changes which cars you buy and how long you hold them.

For investors who want to understand what makes a vehicle worth holding, the collector car definition guide at Butterclassics breaks down appreciation factors clearly.

Key takeaways

Classic cars deliver lower annualized returns than the S&P 500, but their low correlation with equities, tangible asset characteristics, and potential for portfolio diversification make them a legitimate alternative asset for high-net-worth investors with a 5–7 year horizon.

| Point | Details |

|---|---|

| Return gap is real | Classic cars averaged ~4.6% annually vs. ~10% for the S&P 500 between 2018 and 2023. |

| Costs reduce net gains | Annual carrying costs of 2–4% plus 10–15% auction fees significantly cut into appreciation. |

| Tax treatment is unfavorable | The IRS taxes classic cars as collectibles at up to 28%, versus 15–20% for long-term stock gains. |

| Diversification is the real argument | Low correlation with equities makes classic cars valuable for portfolio stability, not raw return. |

| Minimum thresholds apply | Effective direct investment requires ~$500,000 across 3–5 vehicles; funds start at $125,000. |

The numbers are only half the story

I have spent years watching investors approach classic cars the same way they approach growth stocks: they look at the headline return, get excited, and skip the fine print. The fine print is where the real investment case lives.

The classic car market is genuinely maturing. JP Morgan's involvement and the development of indices like the HAGI Top Index signal that institutional money is paying attention. That infrastructure makes the asset class more credible than it was a decade ago. But credibility does not erase the carrying cost problem or the tax disadvantage.

The investors I see succeed with classic cars are not chasing returns. They are high-net-worth individuals who already have strong equity exposure and want a non-correlated, tangible asset they can actually enjoy. A 1969 Chevrolet Camaro Z/28 sitting in a climate-controlled garage is not just a financial instrument. It is something you can drive, show, and pass on. That intangible value is real, even if it does not show up in an annualized return calculation.

My honest advice: if you are comparing classic cars to stocks purely on return, stocks win. If you are building a diversified portfolio and want an asset that does not move with the Nasdaq, a well-chosen classic car makes sense. Know which game you are playing before you write the check.

— Tony

Find investment-grade classic cars at Butterclassics

If you are ready to put this research to work, Butterclassics makes it smooth as butter to find vehicles worth owning.

Butterclassics specializes in investment-grade classic and vintage vehicles, from muscle cars and Corvettes to Broncos and collector trucks. Every vehicle in the inventory goes through a rigorous review process, and Butter Certified vehicles give you the confidence that what you are buying meets a real quality standard. Whether you are adding your first classic car to a diversified portfolio or expanding an existing collection, the Butterclassics team is ready to help you find the right fit. Browse the full classic car inventory today and call dibs on something worth holding.

FAQ

Do classic cars outperform the stock market long term?

Classic cars generally do not outperform the stock market in annualized returns. The S&P 500 returned roughly 10% annually between 2018 and 2023, while classic cars averaged approximately 4.6% over the same period.

What are the biggest risks of investing in classic cars?

The biggest risks are high carrying costs (2–4% annually), illiquidity (4–12 weeks to sell most vehicles), restoration risk (poor work destroys 30–50% of value), and unfavorable tax treatment at up to 28% capital gains.

How long should you hold a classic car investment?

A 5–7 year holding period is recommended to overcome annual carrying costs and allow meaningful appreciation. Short-term holders who bought at the 2021 peak absorbed 20–30% losses during the 2022–2024 down-cycle.

How are classic cars taxed compared to stocks?

The IRS classifies classic cars as collectibles, taxing gains at up to 28%. Long-term stock gains are taxed at 15–20% for most investors. The 2017 Tax Cuts and Jobs Act also eliminated 1031 exchanges for vehicles, removing the only major deferral option.

How much money do you need to invest in classic cars?

Direct investment in a diversified classic car portfolio requires roughly $500,000 spread across 3–5 vehicles. Professional classic car investment funds offer an alternative entry point starting at $125,000.