Offering financing to classic car buyers is a specialized process built around agreed-value appraisals, provenance documentation, and lenders who understand that a 1967 Shelby GT500 is not a depreciating commuter car. The industry term for this niche is collector vehicle financing, and it operates under completely different rules than a standard auto loan. Specialty lenders like JJ Best Banc, LightStream, and Qollateral have built entire product lines around vintage and investment-grade vehicles, recognizing that classic cars appreciate, carry emotional value, and require insurance structures that standard dealership financing simply cannot accommodate. This guide walks you through every financing option, documentation requirement, and loan structure you need to know before signing anything.

What are the main financing options for classic car buyers?

Classic car financing options fall into five distinct categories, and choosing the wrong one can cost you thousands or complicate your title transfer. Here is how each one works.

Specialty classic car loans are the gold standard for collector vehicle financing. Lenders like JJ Best Banc evaluate the vehicle's appraised value, condition, and provenance rather than relying on Kelley Blue Book or Black Book. These loans come with agreed-value appraisals built into the underwriting, which means the lender and borrower agree on the vehicle's worth upfront. This protects you if the car is totaled or stolen.

Personal loans from lenders like LightStream take a completely different approach. LightStream evaluates borrower credit only, ignoring vehicle age, condition, or mileage entirely. This makes personal loans ideal for barn-find projects or unrestored vehicles that would fail a specialty lender's condition requirements. The tradeoff is that no lien is placed on the vehicle, so rates tend to reflect the unsecured nature of the loan.

Bridge financing is the option most collectors overlook. Lenders like Beverly Loan offer liquidity without selling by physically holding your vehicle in a climate-controlled facility during the loan term. You get cash against your collector asset, the car is preserved in secure storage, and you reclaim it upon repayment. These are non-recourse loans, meaning they are not reported to credit bureaus.

Qollateral takes bridge financing further. It offers same-day loans from $50,000 to $2.5 million against investment-grade collector vehicles without traditional credit underwriting or income verification. The vehicle is stored during the loan term and returned in identical condition upon repayment. This structure suits high-net-worth collectors who need liquidity fast without touching their credit profile.

Conventional bank and credit union loans can work for classic cars under $50,000, but most institutions cap loan terms at 60 months and apply standard depreciation assumptions that undervalue collector vehicles. Cash purchases avoid interest entirely but carry opportunity cost and tie up capital that could be deployed elsewhere. Cash works best for sub-$25,000 project cars where appraisal uncertainty makes lenders nervous anyway.

Pro Tip: Before approaching any lender, get an independent appraisal from a certified appraiser affiliated with the American Society of Appraisers or the International Automotive Appraisers Association. A credible appraisal report is the single document that unlocks better loan-to-value ratios and faster approvals.

What documentation do buyers need to secure a classic car loan?

Getting approved for a collector vehicle loan requires more paperwork than a standard auto loan, but the logic behind each requirement is straightforward once you understand what lenders are protecting against.

-

Clean, transferable title. The vehicle must have a clear title with no liens, salvage history, or title washing. Lenders will not fund a vehicle with a clouded title because their collateral position depends on clean ownership transfer.

-

Professional appraisal report. Classic car loans require a professional appraisal because no standard book value exists for collector vehicles. The appraiser documents condition, provenance, restoration quality, and comparable sales. Lenders use this report to set the loan-to-value ratio and confirm they are not overfinancing the asset.

-

Agreed-value insurance policy. Specialty lenders require agreed-value insurance naming them as loss payee. Unlike standard auto insurance, agreed-value policies pay out the full insured amount with no depreciation deduction. Hagerty and American Collectors Insurance are the two most recognized providers in this space.

-

Proof of income and credit documentation. Most specialty lenders require two years of tax returns, recent pay stubs or bank statements, and a credit score above 680. Some lenders, particularly those offering collateral-based bridge loans, skip income verification entirely and focus on asset quality instead.

-

Provenance documentation. Build sheets, Marti Reports for Ford vehicles, Protect-O-Plate cards for GM vehicles, and documented restoration receipts all strengthen your loan application. Lenders prioritize provenance to mitigate valuation risk and confirm the vehicle is what the seller claims it to be.

-

Storage and transport plan. If the lender requires physical possession of the vehicle as collateral, you need to coordinate secure climate-controlled storage and transport logistics before funding. Lenders who hold the vehicle need confirmation that it will be maintained in a condition consistent with its appraised value.

Pro Tip: Order a Carfax and a vehicle history report before your appraisal appointment. Surprises in the vehicle history discovered during underwriting can delay funding by weeks or kill the deal entirely.

How do loan structures for classic cars differ from standard auto loans?

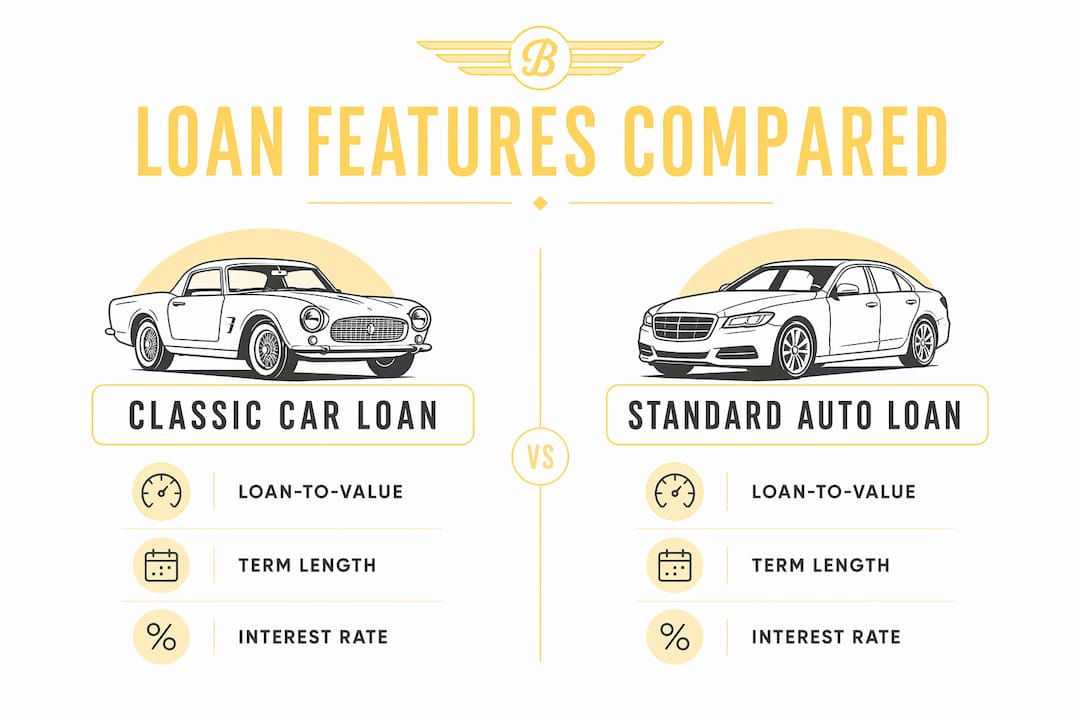

Why financing classic car purchases differs from standard auto lending comes down to three factors: illiquidity, valuation volatility, and the asset's appreciation potential. Standard auto loans assume depreciation. Classic car loans assume the opposite, and the entire structure reflects that.

Loan-to-value ratios are lower. Specialty lenders use conservative LTV ratios typically between 60% and 80% of appraised value. A car appraised at $100,000 might support a maximum loan of $80,000. This buffer protects the lender against sudden market corrections or restoration cost surprises that could erode the vehicle's value.

Term lengths are more flexible. Unlike standard auto loans capped at 72 or 84 months, specialty classic car lenders often offer terms from 12 months to 10 years depending on the vehicle's value and the borrower's profile. Longer terms reduce monthly payments but increase total interest paid, so collectors with strong cash flow often opt for shorter terms.

Interest rates reflect specialty risk. Rates on classic car loans typically run higher than standard auto loan rates because lenders price in appraisal costs, storage logistics, and the illiquid nature of the collateral. Rates vary widely based on credit score, LTV, and lender type.

The table below summarizes the key structural differences:

| Feature | Classic car loan | Standard auto loan |

|---|---|---|

| Loan-to-value ratio | 60% to 80% of appraised value | Up to 100% of MSRP or book value |

| Valuation method | Professional appraisal | Kelley Blue Book or Black Book |

| Insurance requirement | Agreed-value policy required | Standard collision and comprehensive |

| Credit bureau reporting | Sometimes non-recourse, not reported | Always reported |

| Term length | 12 months to 10 years | 24 to 84 months typical |

Leasing and balloon loan structures can be designed to avoid traditional personal credit loan reporting, which matters for collectors managing multiple leveraged assets simultaneously. Balloon loans allow lower monthly payments with a large lump sum due at the end of the term, which works well if you expect the vehicle to appreciate and plan to refinance or sell at maturity.

Practical steps to successfully finance a classic car purchase

Follow these steps in order and you will avoid the most common mistakes collectors make when financing vintage vehicles.

-

Set a realistic total budget. The purchase price is only part of the cost. Factor in taxes, title fees, agreed-value insurance premiums, storage costs, transport, and any planned restoration work. Collectors who budget only for the purchase price often find themselves cash-strapped within six months.

-

Get pre-approved before you shop. Pre-approval from a specialty lender tells you exactly how much you can borrow and at what rate. It also signals to sellers that you are a serious buyer, which matters in a market where desirable vehicles attract multiple offers quickly.

-

Arrange a professional appraisal. Select an appraiser with documented experience in the specific marque you are buying. A generalist appraiser who does not know the difference between a numbers-matching engine and a replacement block will produce a report that specialty lenders reject.

-

Verify provenance and title. Confirm the VIN matches all documentation, review the title for any liens or salvage notations, and collect every piece of supporting documentation the seller has. Gaps in provenance history are negotiating leverage and financing risk at the same time.

-

Compare lenders on four criteria. Rate, LTV ratio, funding timeline, and storage requirements are the four variables that matter most. A lender offering a slightly lower rate but requiring 30 days to fund may cost you the vehicle if a competing buyer can close in a week.

-

Secure agreed-value insurance before closing. Contact Hagerty or American Collectors Insurance, provide the appraisal report, and get a policy in place that names your lender as loss payee. Most specialty lenders will not release funds until proof of insurance is confirmed.

-

Close with a clean lien recording. At closing, confirm the lender's lien is properly recorded on the title in your state. This protects both parties and is required before the lender releases funds to the seller.

Pro Tip: Ask your lender whether their loan is recourse or non-recourse before signing. Non-recourse loans are not reported to credit bureaus and do not expose your personal assets if the vehicle's value drops below the loan balance. For collectors with multiple financed assets, this distinction is significant.

Key takeaways

Collector vehicle financing requires agreed-value appraisals, specialty lenders, and loan structures built around appreciation rather than depreciation.

| Point | Details |

|---|---|

| Use specialty lenders | JJ Best, Qollateral, and Beverly Loan understand collector vehicle valuation in ways banks do not. |

| LTV ratios run 60% to 80% | Budget for a meaningful down payment; classic car lenders do not fund at full appraised value. |

| Agreed-value insurance is mandatory | Secure a Hagerty or American Collectors policy naming your lender as loss payee before closing. |

| Provenance documentation matters | Build sheets, Marti Reports, and restoration receipts directly affect your loan approval and rate. |

| Non-recourse loans protect your credit | Bridge financing structures from lenders like Beverly Loan and Qollateral do not appear on credit reports. |

Why I think most collectors underestimate financing risk

I have seen collectors walk into a purchase with a solid appraisal, a pre-approval letter, and a beautiful car, and still end up in trouble six months later. The issue is almost never the loan itself. It is the costs that show up after the paperwork is signed.

Restoration surprises are the biggest threat to a financed classic car. A vehicle appraised at $120,000 can absorb a $15,000 mechanical issue and still hold its value. But if you borrowed $90,000 against it and the repair bill arrives before your first payment, your liquidity position gets uncomfortable fast. Conservative LTV ratios exist for exactly this reason, and I think buyers who push lenders for maximum financing are taking on risk they have not fully priced.

The other thing I would push back on is the assumption that cash is always safer. Collectors should weigh interest costs against the opportunity cost of liquidating other assets, considering tax impacts and expected appreciation horizons. A well-structured specialty loan that preserves your liquidity while the vehicle appreciates is often the smarter financial move, not the riskier one.

Non-recourse bridge financing is genuinely underused by collectors who do not realize it exists. If you own a vehicle worth $200,000 and need $80,000 for another opportunity, pledging the car through a lender like Qollateral or Beverly Loan gets you that capital without selling, without touching your credit, and without a tax event. That is a tool worth knowing about.

— Tony

Find your next classic car at Butterclassics

Ready to put what you have learned into practice? Butterclassics makes the buying side of this process smooth as butter. Browse a hand-picked inventory of investment-grade muscle cars, Corvettes, Broncos, vintage trucks, and more, all with detailed specs and high-quality photos so you know exactly what you are getting.

Butterclassics also offers financing pre-qualification directly through the site, so you can check your options before you fall in love with a specific car. Every vehicle in the Butter Certified inventory has been vetted for quality, giving you the documentation foundation that specialty lenders want to see. Whether you are a first-time collector or adding to an established portfolio, the team at Butterclassics is ready to help you drive home in something worth owning.

FAQ

What credit score do you need for a classic car loan?

Most specialty classic car lenders require a credit score of at least 680, though collateral-based lenders like Qollateral skip credit checks entirely and evaluate the vehicle's value instead.

Do classic car loans require a down payment?

Yes. Because specialty lenders use LTV ratios of 60% to 80%, buyers typically need a down payment of 20% to 40% of the appraised value depending on the lender and vehicle.

Can you finance a classic car that needs restoration?

Personal loans from lenders like LightStream can finance project cars regardless of condition because they evaluate borrower credit only. Specialty collateral lenders generally require the vehicle to be in drivable or show condition.

Is agreed-value insurance required for classic car financing?

Specialty lenders require agreed-value insurance policies naming them as loss payee. Hagerty and American Collectors Insurance are the most widely accepted providers in this category.

What is a non-recourse classic car loan?

A non-recourse loan uses the vehicle as the sole collateral, meaning the lender cannot pursue your personal assets if the vehicle's value falls below the loan balance. These loans are typically not reported to credit bureaus, making them attractive for collectors managing multiple financed assets.